This means that you are loosing your retirement savings by thousands every year. I know, because I used to do it as well.

In my professional experience dealing with clients, the ones who had no clue about interest rates were the ones who were shocked into temporary shame.

Roger, a client of mine was a good guy, he paid his bills on time. But he didn’t have the financial education that he needed, and he paid too much for his lack of financial education.

Rogers’ lack of knowlege was costing him $220 a month in minimum payments.

I told Roger that he was only paying 2.11% of his $10,300 of debt. Roger asked me “why would they [the credit card company] do that to me? I’ve paid them on-time, every month, for over 13 years!” I replied, “it’s not personal Roger, it’s business.”

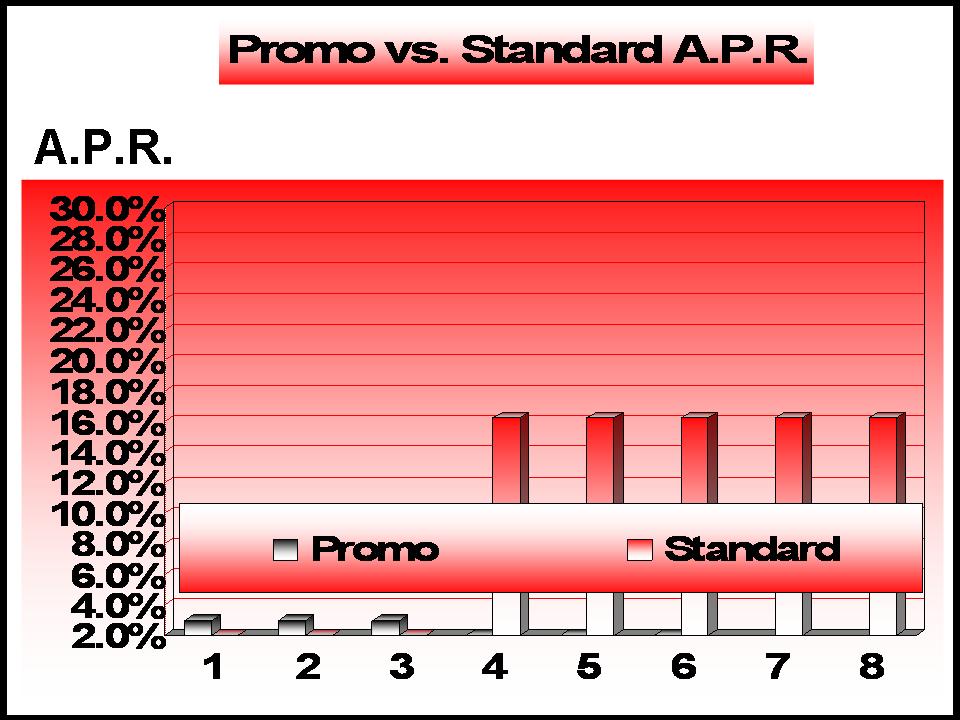

The Mark-up

You know the way that stores buy products from Wholesalers and then “tack on” their cost before they sell it to you? It’s the same way with Interest Rates. Just like in a store. Some prices on products are better than others.

Credit Cards offer products that they later tack extra interest on. Sometimes these fees are excessive and other times down right abusive.

But the end is comming. The “Anti-Debt Revolution” as begun. Bookmark us for updates.

Support the War On Debt. Send us your comments and or questions.

Media inquires? email: Jford@debtwarriors.com.

Wishing you financial security. We are Debt Warriors!